ESOP is short for an Employee Stock Ownership Plan and is an employee retirement plan as well as a technique of corporate finance. An ESOP can be used to finance the transition of ownership, raise new equity capital, refinance outstanding debt or acquire productive assets. ESOPs can also be used to increase cash flow by making plan contributions in stock instead of cash.

One of the most common reasons for establishing an ESOP is to buy stock from the owner(s) of a closely held company to create an exit strategy. Shareholders can sell all their shares at one time or schedule to sell percentages of their shares in the business to the ESOP. This gives a business owner the flexibility to structure their transition of leadership and business exit.

The ESOP is designed to be a shareholder of the company alongside its role of providing retirement benefits to employees. Unlike other retirement plans, the ESOP can borrow money to purchase employer stock, allowing it to accumulate significant amounts of stock. In addition, several special tax benefits incentivize business owners to sell stock to the ESOP.

How an ESOP Works

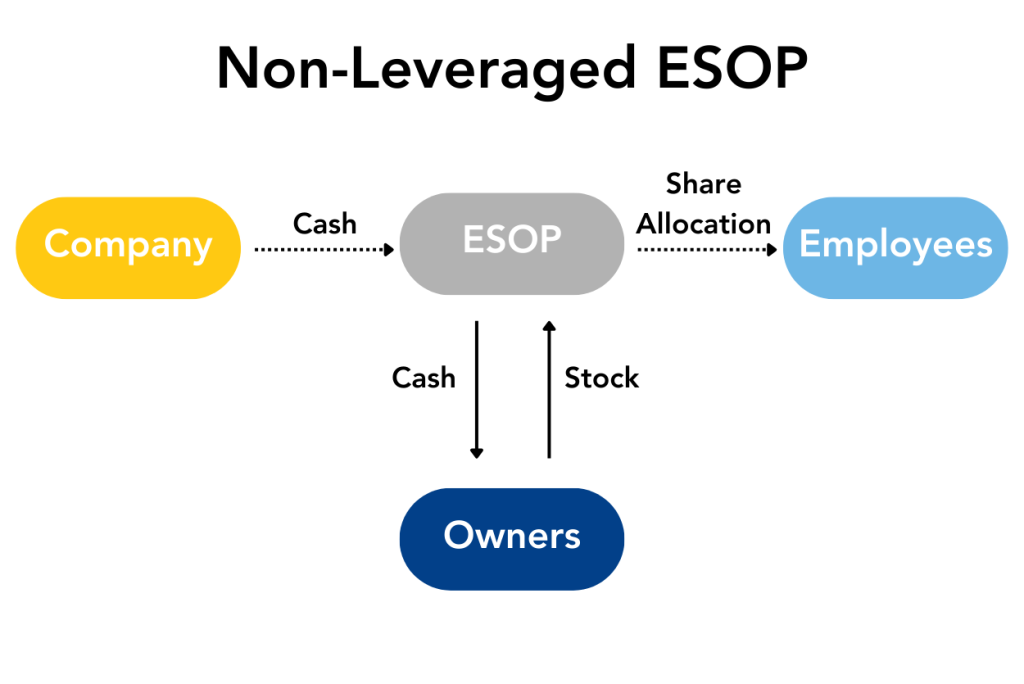

The ESOP provides participants with ownership in their employer. To accomplish this, the company sets up a trust for the principal purpose of acquiring and holding securities or stocks for the benefit of its employees.

This is the basic form of creation for an ESOP in terms of the transaction, but creating the plan is a bit more complex. It requires a legal team well-versed in ERISA Law (defined in the Employee Retirement Income Security Act), a third-party administrator, trustees, corporate lawyers, individual’s lawyers, valuation specialists, and possibly lenders—quite a troop.

ESOP is one of a handful of options for business owners to consider when planning their business exit strategy, as an ESOP provides a ready market for some or all the shares owned by shareholders in a closely held company. With an ESOP in place, a majority or controlling shareholder has an exit strategy when they are ready to retire by transferring company shares. For this reason, an ESOP is also an attractive buyer for a minority shareholder in the business.

ESOP costs are much like those associated with a third-party sale in the year of sale. However, the company will incur ongoing periodic costs of maintaining an ESOP. These ongoing costs would not typically occur in a third-party sale and include costs for trustee fees, annual valuations, audits, and other professional fees. The ongoing costs are paid from the future earnings and should be included in a feasibility study. The feasibility study is one of the first steps to establishing an ESOP. Basically, it considers the pros and cons of the specific business and is performed to determine if the ESOP is a reasonable alternative. Generally, the question answered by the feasibility study is, “Does it work?” Maintenance of positive annual cash flow from operations will indicate it as a viable alternative.

Attractive Business Qualities

While the Feasibility Study looks specifically at key financial aspects of the business, there are several qualities to help owners determine if an ESOP could be the ideal exit solution. This includes:

- Company has strong cash flow

- Company has a history of increasing sales and profits

- Company is in a high federal income tax bracket

- Company is not heavily leveraged and has substantial stockholder equity

- Company has capable second-line management in place

- Company has 30 or more employees

- Company has more than $5 million in annual sales

Consider the Employee-Owned Aspect

In addition to analyzing the financial aspects of an ESOP as an exit strategy, it’s also important to consider the employees. Proponents of employee ownership emphasize the incentive and team-building advantages of paying employees in part with employer stock. Critics argue that concentrating employees’ financial resources in their employer’s securities increases their exposure to their employer’s fortunes. The future success of the company will be partly dependent on the employee culture and mindset.

The ESOP Association performed a study of its members and found that most of its members reported increased productivity and improved employee morale. A study by the National Center for Employee Ownership found that ESOP companies grew more than 5% a year faster than their non-ESOP counterparts.

Tax Considerations

Although there are numerous aspects of an ESOP to consider when forming an ESOP, income tax issues are important. Depending upon the corporate form at the time of the sale of the shares to the ESOP, there are certain issues of which you should be aware. The high points are:

For C-corps:

- The sale of more than 30% of the outstanding shares to the ESOP allows the shareholders to elect deferral of the gain and, therefore, the income tax on the gain if they invest the proceeds in “qualified replacement property.”

- Annual contributions to the ESOP are tax deductible as employee benefit plan expenses equal to at least 25% of covered payroll, possibly more if the ESOP is leveraged.

- The TCJOA changed the rules surrounding the deduction of interest paid on corporate loans, and the limitations may possibly affect leveraged ESOPs and the deductibility of loan interest.

For S-corps:

- The income and gain passthrough to the ESOP trust is non-taxable as the ESOP is a non-taxable entity. This benefit is termed a “tax shield.”

- Employer contributions to the ESOP are limited to a maximum of 25% of covered payroll, whether leveraged or not.

- Deferral of the gain on sale of the shares by the shareholder is not allowed.

Rivero, Gordimer & Company Specializes in Business Succession Planning

Rivero, Gordimer & Company is well-positioned to assist with all aspects of succession planning, including valuations, mergers and acquisitions, and ESOPs. Our team partners with businesses across a variety of industries. When it comes to the transition of ownership, our team has assisted with countless ownership transitions through gifting, sale to third parties, and ESOPs. Partner with RGCO to ensure that closing the business you’ve worked so hard to build is not an option.